Your QSEHRA Starting Point

Start here if you're considering a QSEHRA for your small business. This video explains what a Qualified Small Employer HRA is, how tax-free health insurance and medical expense reimbursements work, who qualifies, and how to set up and administer a QSEHRA through Salusion. By the end, you'll understand how to create your HRA, set employee allowances, and offer a simple, affordable health benefit.

QSEHRA Administrator Comparison

Why Businesses Choose Salusion

Simple, Low-Cost QSEHRA Pricing

No setup fees. No platform fees. No minimums. Salusion makes QSEHRA administration simple, transparent, and affordable for small businesses.

Easy to Set Up. Easier to Administer.

Set up your QSEHRA in 15 minutes. From compliance to expense tracking to reimbursements, Salusion automates the administrative work. With ACH reimbursements built in, you can offer a small-business HRA while spending almost no time managing it.

Built-In Employee Insurance Enrollment

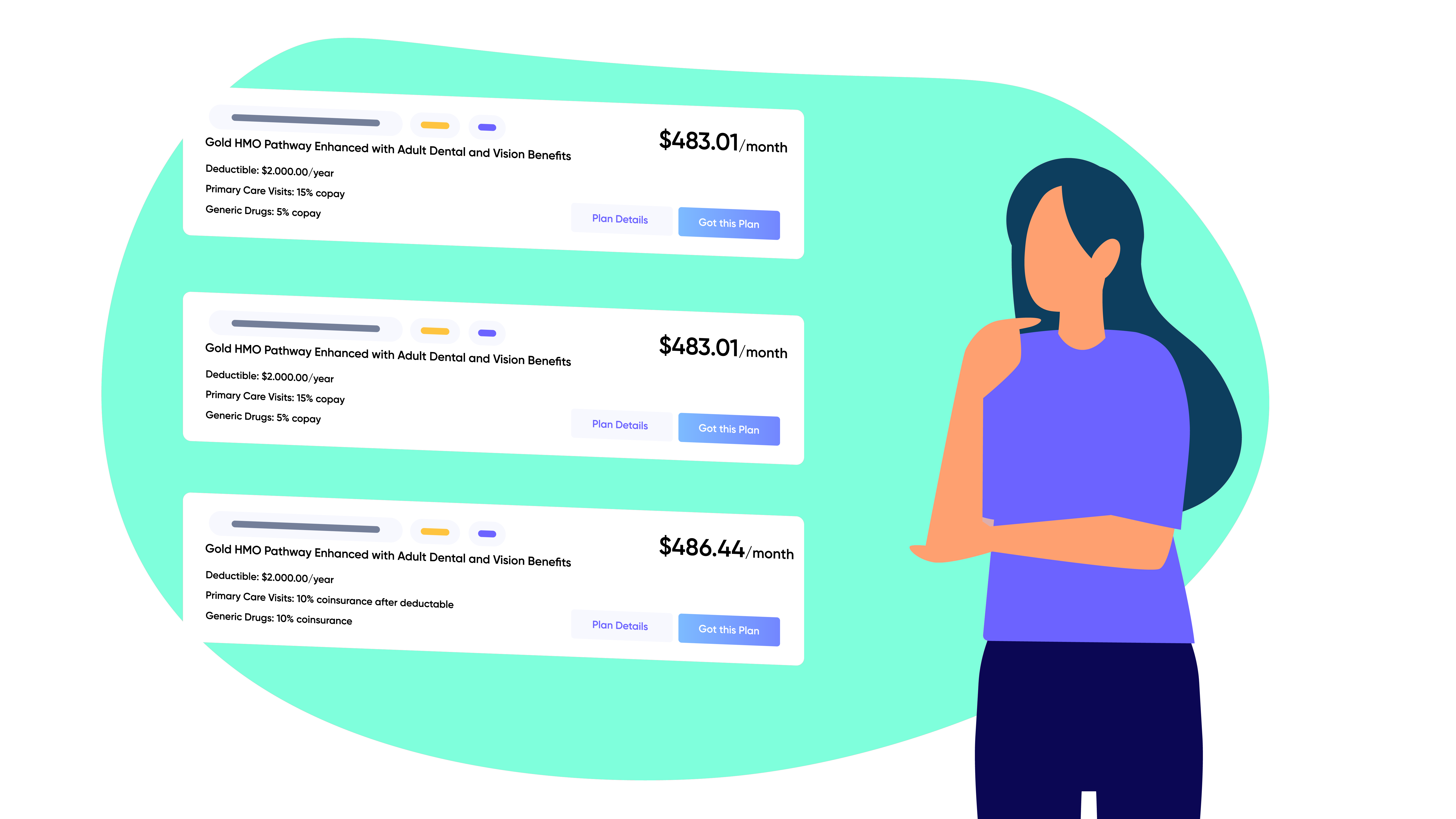

Employees can compare plans and purchase individual health insurance directly through Salusion, making it easier for them to use their QSEHRA allowance with confidence.

Real People. Expert Support.

Most emails are answered in under an hour. Same-day Zooms with a QSEHRA expert give employers and employees confidence their issue will be solved quickly and completely.

What Customers Say

Want to Learn More About QSEHRAs?

These short guides answer the first questions most small employers ask before setting up a QSEHRA: what it is, whether your business qualifies, and how employee reimbursements work.

What Is a QSEHRA?

Learn how a Qualified Small Employer HRA helps small businesses reimburse employees tax-free for individual health insurance premiums and eligible medical expenses - without offering a traditional group health plan.

Who Can Sponsor a QSEHRA?

Find out whether your small business is eligible to offer a QSEHRA, including the employee-size rules, group health plan restrictions, and key requirements to know before creating your HRA.

How Does a QSEHRA Work?

Understand the basic mechanics of a QSEHRA plan year, including employee allowances, monthly reimbursements, eligible claims, unused allowances, and how employees get reimbursed through Salusion.

QSEHRA Planning Tools

Before you create your QSEHRA, use these tools to answer the two questions small employers ask most: how much should you offer, and what will individual health insurance cost your employees?

How Employers Set QSEHRA Allowances

Benchmark your QSEHRA allowance against real employers on Salusion. See the most common allowance designs, average monthly reimbursement amounts, and how businesses decide between a flat allowance, family-size allowance, or age-based QSEHRA structure.

Estimate Employee Health Insurance Costs

Estimate the average cost of individual health insurance based on an employee's ZIP code and age. Use the results to choose a QSEHRA allowance that fits your budget and gives employees a realistic view of what their reimbursement can cover.

Frequently Asked Questions

ICHRA vs. QSEHRA: Which HRA is right for your business?

A QSEHRA is usually best for small employers with fewer than 50 full-time equivalent employees that want a simple, tax-free reimbursement benefit. An ICHRA can work for employers of any size and offers more flexibility by employee class, with no annual IRS reimbursement limit.

Read the full article →Can a QSEHRA reimburse employees without health insurance?

No. Employees must have Minimum Essential Coverage, or MEC, before they can receive QSEHRA reimbursements. Without qualifying coverage, reimbursements cannot be made through the QSEHRA.

Read the full article →What are the 2026 QSEHRA contribution limits?

For 2026 plan years, employers can reimburse up to $6,450 for self-only coverage and $13,100 for family coverage. Employers can choose lower allowances, and Salusion helps track reimbursements against the annual QSEHRA limits.

Read the full article →Can business owners participate in a QSEHRA?

It depends on the business structure. C-corporation owner-employees can generally participate, while sole proprietors, partners, LLC members taxed as partners, and more-than-2% S-corporation shareholders generally cannot receive tax-free QSEHRA reimbursements.

Read the full article →How do QSEHRAs affect premium tax credits?

Employees offered a QSEHRA must report the benefit to the Marketplace. If the QSEHRA is affordable, the employee generally cannot claim a premium tax credit. If it is not affordable, the employee may still qualify, but the credit is reduced by the QSEHRA allowance.

Read the full article →What expenses are eligible for QSEHRA reimbursement?

QSEHRAs can reimburse individual health insurance premiums and other eligible medical expenses under IRS Section 213(d), including many out-of-pocket costs such as deductibles, copays, coinsurance, and prescriptions. Employers can choose which eligible expense categories their QSEHRA will cover.

Read the full article →